The Iran-centered conflict may not continue at its current intensity for much longer.

That is the good news.

The more important question for the cruise industry, however, is this:

What happens after the acute phase ends, but the commercial aftershocks continue moving through the system?

That is where strategy matters.

My view is that the immediate operational damage is concentrated in the Persian Gulf and nearby Eastern Mediterranean. That is where the disruption is most visible: ships trapped in the Gulf, disrupted Europe-Asia air corridors, elevated travel warnings, itinerary changes, future cruise cancellations, and difficult fleet redeployment decisions.

But the longer-lasting impact will not be limited to that immediate geography.

It will be felt more broadly through fuel prices, airfares, travel psychology, booking hesitation, and the time it takes for consumer confidence to rebuild.

That is the strategic layer beneath the headlines.

Travel is a confidence business.

Cruising, in particular, is not just about ships. It is about an interconnected system: airlift, timing, fuel, insurance, perception of safety, and the consumer’s willingness to commit money well in advance. When one part of that system becomes unstable, the effects travel far beyond the original point of disruption.

That is why I do not believe this event points to a broad collapse in cruise demand.

I believe it points instead to demand diversion, delayed commitment, and a longer recovery arc for certain regions than many may initially expect.

Consumers Do Not Buy Geography. They Buy Confidence.

That confidence rests on a few practical questions:

Will my itinerary operate as planned? Will my flights work? Will costs continue to rise after I book? Will the region still feel stable by the time I travel? If things change, will I be protected?

When uncertainty rises, consumers rarely all respond in the same way. Some cancel. Some postpone. Some wait. Many simply choose another destination that feels easier, safer, and more predictable.

That is why the sharper distinction right now is not between people traveling and people not traveling.

It is between people still traveling and where they now prefer to travel.

That matters a great deal.

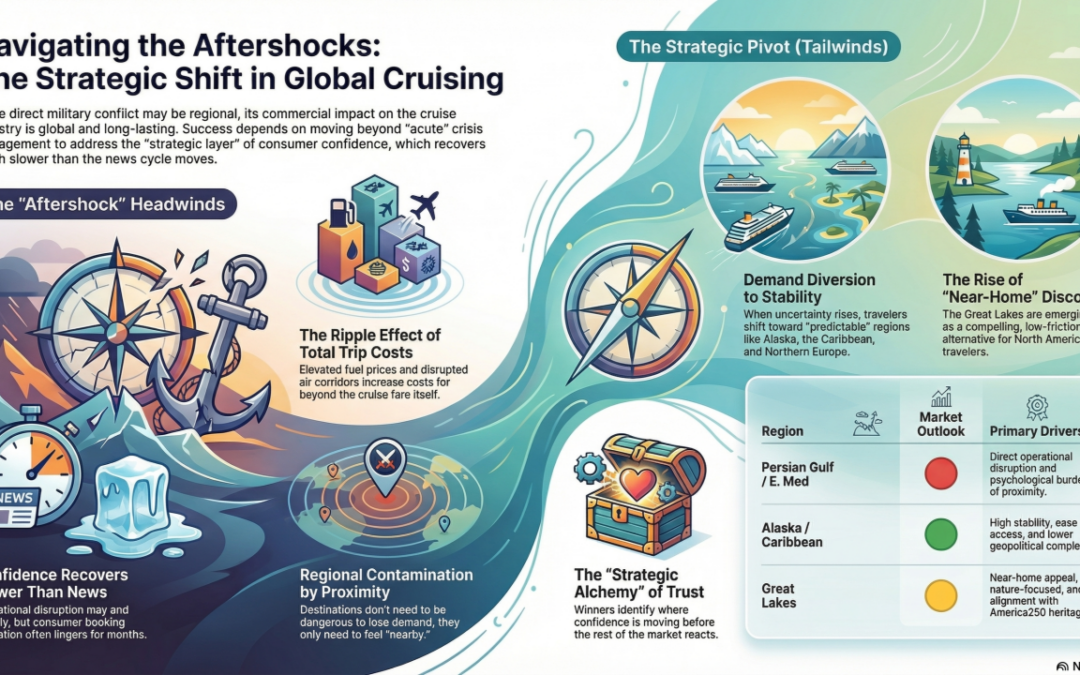

The Gulf and nearby Eastern Mediterranean face the heaviest headwinds because they are bearing both the direct operational consequences and the wider psychological burden of proximity to conflict. Even after hostilities moderate, recovery will likely take longer than many assume because confidence does not rebound as quickly as the news cycle moves on.

Why the Aftereffects Will Outlast the Acute Phase

There are several reasons.

First, travel planning has lead times. Cruises, especially fly-cruise vacations in Europe and beyond, are often booked months in advance. When a consumer becomes hesitant during the booking window, that hesitation can linger long after the most dramatic headlines fade.

Second, fuel effects outlast military intensity. Even if oil retreats from peak levels, that does not necessarily mean a quick return to pre-conflict travel economics. Airlines and cruise operators absorb and pass through fuel costs on different timelines. Higher fuel can continue shaping airfares and operating costs well after the conflict cools.

Third, air access matters more than many realize. The Europe-Asia corridor is a critical piece of the global travel system. If it remains disrupted, longer, more expensive, or less predictable, the effect reaches well beyond the conflict zone itself. It changes the economics and emotional appeal of many long-haul travel decisions.

Fourth, government advisories cast a long shadow. Even when travelers understand that a particular destination is not in the center of the conflict, elevated warnings and broad cautionary language can influence perception across a much wider field.

This is why I believe the aftereffects will be broad even if the battlefield remains geographically contained.

The Headwinds

The first is higher total trip cost.

Consumers do not evaluate a cruise fare in isolation. They evaluate the full cost of the vacation: airfare, hotels, transfers, insurance, excursions, and onboard spending. If airfares remain elevated, many cruise vacations become more expensive even when the cruise itself still looks like relatively good value.

The second is hesitation.

Not panic. Hesitation.

That may prove to be the more consequential force. A consumer who waits for greater stability and predictability is not lost forever, but that delay weakens booking curves, pressures pricing, and complicates deployment decisions.

The third is regional contamination by proximity.

A destination does not need to be dangerous to become commercially vulnerable. It only needs to feel nearby, complicated, or exposed to the same narrative.

The fourth is itinerary instability.

Travelers want confidence that the cruise they are booking is the cruise they will actually take. The more consumers worry about substituted ports, changed embarkation points, or shortened programs, the more attractive simpler alternatives become.

The fifth is margin pressure for cruise lines.

They may face higher fuel, disrupted schedules, lost revenue in exposed programs, compensation costs, and less efficient redeployments.

The Tailwinds

This is not only a story about headwinds.

It is also a story about where confidence goes next.

Whenever confidence recedes in one part of the market, it gathers somewhere else.

The likely beneficiaries are the destinations and itineraries that score well on a few simple but powerful attributes: they feel stable, are easier to reach, carry less geopolitical complexity, and are easier for the consumer to understand.

That creates a meaningful demand tailwind for:

- Western Europe

- Northern Europe

- Alaska

- The Caribbean

- Canada/New England

I would add something else that deserves more attention:

The Great Lakes: An Emerging Near-Home Alternative

The Great Lakes are emerging as an especially compelling near-home small ship cruise alternative.

That matters for several reasons.

The Great Lakes offer a combination that aligns well with the mood of the moment: nature, culture, history, manageable complexity, and close-to-home appeal for North American travelers.

They also fit beautifully with the spirit of America250, as the United States approaches its 250th anniversary. For many travelers, that milestone will increase interest in destinations that combine celebration, heritage, and meaningful exploration closer to home.

That makes the Great Lakes more than a niche product.

It makes them part of a broader strategic pattern:

When global uncertainty rises, near-home discovery becomes more compelling.

In that sense, the Great Lakes may benefit not only from current geopolitical disruption, but also from a larger cultural and consumer shift toward immersive, lower-friction travel experiences rooted in nature, history, and regional identity.

What Cruise Lines Are Likely To Do

From the cruise line perspective, the logic is straightforward.

First, protect guests and crews. Second, cancel or modify what cannot operate reliably. Third, preserve pricing and confidence where demand remains positive. Fourth, redeploy movable capacity toward regions with stronger demand and better operating stability. Fifth, be slower to recommit capacity to regions where confidence, air access, and pricing remain unstable.

In short, the strategic issue is not simply whether the conflict continues.

It is whether confidence returns fast enough to restore normal planning behavior.

That will likely take longer than the conflict’s most intense phase.

Operational disruption may fade first. Consumer confidence may recover second. Itinerary restoration may follow after that. And pricing normalization may take longer still.

The Strategic Takeaway

The direct shock may be regional.

The aftereffects will be broader.

And the winners will likely be the destinations, itineraries, and brands that best align with what travelers value most in uncertain times:

clarity, confidence, accessibility, and trust.

That is the Strategic Alchemy in this moment—understanding that when disruption narrows confidence in one geography, it can widen opportunity somewhere else.

The key is seeing where confidence is moving before everyone else does.

➡️ Let’s connect. Send me a message or email me directly: david@globalvoyagesgroup.com

David Giersdorf Advisor | Strategist | Author of Hard Ships | Creator of The Business Resilience Framework | Former CEO & Industry Leader.