The most interesting action in cruise today isn’t on the mega‑ship side. It’s in the niche segments: luxury, expedition, yacht, and river.

It’s also where the ownership picture is most misunderstood.

Executives and advisors know the brands. They rarely see the capital and strategy behind those brands. Yet ownership drives ship orders, itineraries, risk appetite, distribution strategy—and ultimately, which products survive the next down‑cycle.

In this Strategic Alchemy note, I map the ownership architecture of niche cruising and highlight what it means for leaders, investors, and advisors.

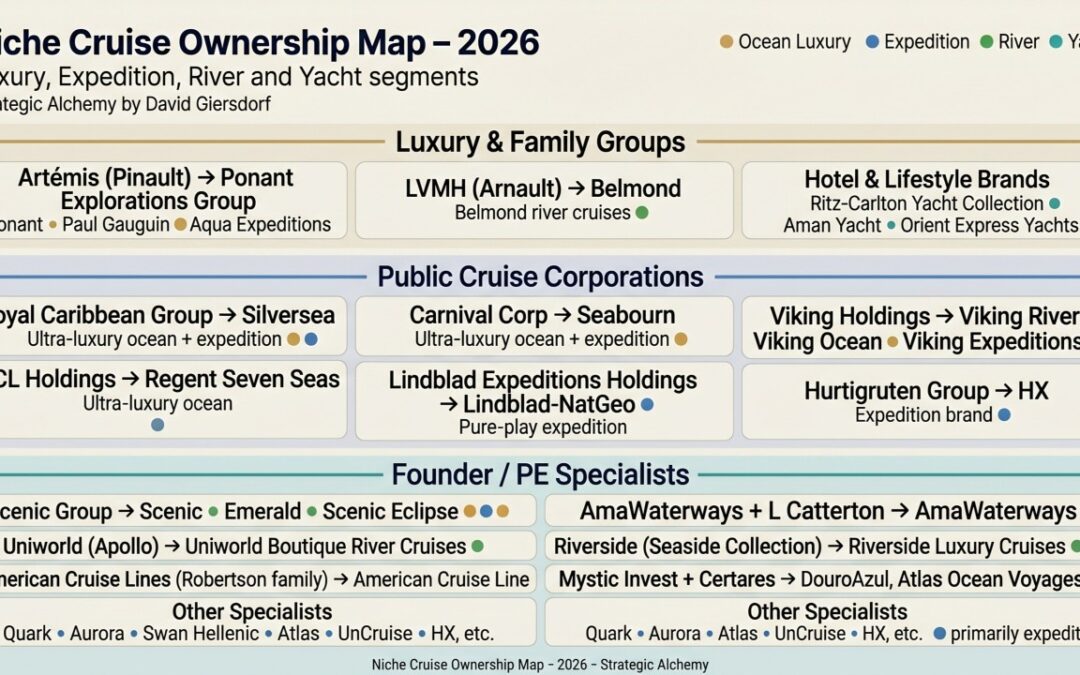

1. Three owner archetypes behind niche cruising

When you zoom out across luxury, expedition, and river, three distinct ownership types shape the category.

1) Luxury groups and family holding companies

These owners treat cruise as one asset class inside a broader luxury ecosystem:

- Artémis (Pinault family)

- LVMH (Arnault family)

- Hotel and lifestyle groups extending offshore

This is where fashion, hospitality, and family capital meet at sea.

2) Public cruise corporations

These owners integrate luxury and expedition into larger, diversified cruise portfolios:

- Royal Caribbean Group → Silversea (including Silversea Expeditions).

- Carnival Corporation → Seabourn (ocean and expedition).

- Norwegian Cruise Line Holdings → Regent Seven Seas Cruises.

- MSC Group → Explora Journeys (luxury ocean/yacht).

- Viking Holdings → Viking River, Viking Ocean, Viking Expeditions.

- Lindblad Expeditions Holdings → Lindblad–National Geographic (pure‑play expedition).

- Hurtigruten Group → HX (Hurtigruten Expeditions), the dedicated expedition brand.

For these groups, niche cruising is a portfolio segment with specific yield and brand objectives.

3) Founder, family, and PE‑backed specialists

This is the long tail of highly focused platforms, often founder‑led and backed by family or private equity:

- Scenic Group → Scenic Luxury Cruises & Tours, Emerald Cruises, and Scenic Eclipse discovery yachts.

- AmaWaterways → Founders Schreiner/Karst/Murphy plus a significant growth stake from L Catterton.

- Uniworld Boutique River Cruises → Now under Apollo via The Travel Corporation.

- Riverside Luxury Cruises → Gerlach family’s Seaside Collection (ex‑Crystal river fleet).

- Century Cruises → Century River Cruises on the Yangtze, with growing ambitions into other rivers.

- American Cruise Lines → Robertson family, U.S.‑flag river and coastal.

- DouroAzul / Mystic Invest → Ferreira family + Certares, powering Douro and broader expedition/river capacity.

- SeaDream Yacht Club → Family‑owned yacht line (SeaDream I & II) from Seabourn’s original founder.

- Expedition specialists like Quark, Aurora, Swan Hellenic, Atlas, UnCruise, Heritage Expeditions, Oceanwide, and others.

Each archetype plays a different game. That’s where the strategic signal is.

2. Ownership as a proxy for risk and innovation

Public groups must defend every expedition newbuild and itinerary to public markets. They optimize for:

- Flexible ships that can move between regions and segments.

- Tight alignment with loyalty programs and private‑island ecosystems.

- Scaled, repeatable deployment patterns and clear return thresholds.

Their luxury and expedition brands are portfolio components, not existential bets.

Founder, family, and PE platforms behave differently:

- They can back smaller, more specialized ships and highly differentiated itineraries.

- They lean into science, education, and story without needing everything to scale to thousands of berths.

- They can move faster into new regions or formats—think discovery yachts, hybrid sail power, and more immersive land programs.

Hotel and lifestyle owners (Ritz‑Carlton, Four Seasons, Aman, Orient Express, Sea Cloud, SeaDream) are playing yet another game: brand halo and ultra‑high‑yield yield. Capacity is limited; signaling power is not.

Every time you evaluate a brand, ask: What is the owner really optimizing for—EPS, family legacy, brand equity, or a future transaction?

3. Asset owners vs product owners: who actually controls the experience?

In expedition and river, the company that owns the steel is often not the company that owns the product.

Examples:

- Abercrombie & Kent Expedition Cruises traditionally chartered ships while owning the itinerary, onboard program, and guest relationship—even before acquiring Crystal and its ships.

- Lindblad owns and operates vessels, while National Geographic contributes content, brand, and distribution.

- DouroAzul/Mystic and Century build and/or operate ships that sail under other brands’ flags on the Douro, Nile, Yangtze, and beyond.

Implications:

- Brand risk and continuity sit with the product owner.

- Capital risk and operational resilience sit with the asset owner.

When cycles turn, charters get reshuffled, partnerships re‑papered, and ships rebranded faster than most realize. If your strategy is built around “Brand X” but you don’t know who owns the hull and the debt underneath, you’re flying partially blind.

4. River: more consolidated than it looks

River feels fragmented, but at the upper‑premium and luxury end, capacity clusters around a surprisingly small set of platforms:

- Viking River as the scaled, founder‑controlled global platform.

- Scenic + Emerald as a privately held luxury/deluxe river and yacht ecosystem.

- AmaWaterways as a classic founder + PE hybrid, with L Catterton funding growth.

- Uniworld under Apollo’s ownership, with its boutique, art‑driven ships.

- Riverside Luxury Cruises as the reborn Crystal river fleet.

- Avalon Waterways under the Globus family of brands.

- Tauck River Cruises, with Tauck controlling the guest experience and Scylla operating ships.

- Riviera River Cruises (UK‑centric).

- American Cruise Lines, owning the modern U.S. riverboat and coastal niche.

- DouroAzul/Mystic and Century Cruises, which not only run their own ships but also power or white‑label vessels for Western brands on the Douro, Nile, Yangtze, and other rivers.

To destinations, it looks like dozens of logos. Strategically, you are dealing with a handful of owner platforms that control most of the high‑yield berths.

5. Luxury expedition and yacht: an asset class inside luxury ecosystems

Luxury expedition and yacht‑style cruising have matured into a true asset class inside broader luxury ecosystems:

- Fashion and luxury families (Pinault via Artémis, Arnault via LVMH/Belmond) are building seagoing platforms that complement their maisons, wineries, and art holdings.

- Hotel and lifestyle brands (Ritz‑Carlton, Four Seasons, Aman, Orient Express, plus Sea Cloud and SeaDream) are developing and operating small fleets of ultra‑luxury vessels that function as mobile branded villas.

- Cruise corporations (Royal, Carnival, MSC, Viking) are integrating expedition into their larger loyalty, deployment, and private‑island strategies.

This shifts the power map:

- Expedition is no longer just a niche category. It’s a strategic lever for deepening relationships with the most valuable guests—those who buy suites, villas, and private aviation.

- Control of hardware, itineraries, and guest data is concentrating in the hands of a few groups that can connect sea, land, and brand end‑to‑end.

The winners will treat expedition and yacht not as inventory, but as influence over the affluent traveler’s lifetime journey.

6. Implications for leaders and advisors

Four practical takeaways:

- Map ownership before you commit. When you sign a partnership, allocate marketing dollars, or build product around a niche brand, you are really aligning with the owner behind it. Understand their capital structure, horizon, and exit logic.

- Expect more consolidation and “brand migrations.” Some boutique names will disappear or move platforms as the cycle evolves. Platforms—ships, crews, distribution contracts—often survive under new flags. Build optionality into how you partner and promote.

- Segment by ownership, not just by ship. Cabins and inclusions are the visible layer. Ownership tells you how the product is likely to evolve over the next 3–5 years, and how it will behave under stress.

- Watch the hotel‑yacht and tall‑ship segment. Ritz‑Carlton, Four Seasons, Aman, Orient Express, Sea Cloud, SeaDream and similar players won’t dominate capacity, but they will heavily influence expectations on design, personalization, and integration across land and sea.

7. A working tool: the Niche Cruise Ownership Table

To make this usable, I’ve built a working table that maps:

- Owner type (public, family, PE, hotel/lifestyle).

- Parent / holding company.

- Platform (Ponant Explorations Group, Scenic Group, Viking Holdings, Mystic Invest, The Yacht Portfolio, etc.).

- Consumer brands across luxury, expedition, river, and yacht.

- Segment flags (ocean luxury, expedition, river, yacht).

I use this as a living reference in my advisory work with cruise lines, hotel brands, destinations, and investors.

If you’d like a copy of the current version, add the word “ownership” in the comments and I’ll send you the link.

8. How I support leaders in this space

Through Global Voyages Group, I provide bespoke C‑suite advisory and consulting services to cruise lines, hotel brands, destinations, and investors, with a particular focus on luxury, expedition, yacht, and river segments. Drawing on our proprietary Bristol Affluent Traveler Marketing Database, we also support targeted revenue generation and audience development across these sectors.

Reach out to me directly. I’m always open to a focused conversation about where you are today, where the market is going, and how to bridge that gap.